|

We offer:

Implementation of Quality Control Comply Eye Services creates and assists in implementing Quality Control Plans, Fair lending plans, due diligence plans, reviews & training for pre and post closing in an effort to protect the quality and integrity of the origination, processing and underwriting procedures throughout mortgage transactions. The programs and procedures are designed to assure that compliance with all regulations are followed and all policies and requirements of state and federal agencies are adhered to, as well as all policies and requirements of investors, insurers and sponsors. Implementation of the specific plans starts with required closed, rejected/denied, early default, etc. reviews on a monthly basis. Comply-Eye Services works along side clients to address and assist in planning and assembling training in those areas of deficiencies for pre & post closing practices. Clients get to design their own plan using past and/or present corrective actions. Corrective actions are performed by the client following Comply Eye monthly, quarterly and yearly reports in an effort to protect the integrity of the loan files. Once corrective actions have be performed, those corrective actions will be added to the Quality Control Plan Procedures manual. What ever your quality control needs, Comply-Eye Services either has a plan ready for you or we can customize a plan based on your specific needs. |

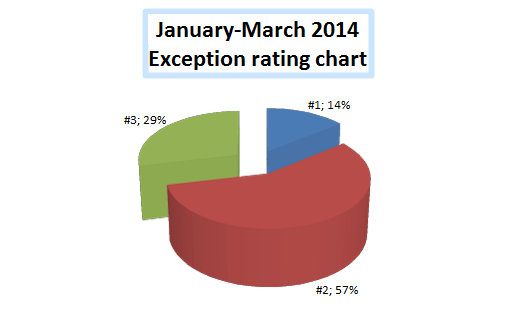

We provide clients with charts so they can get the complete scope of the quality control reviews.

Example of a monthly exception rating chart.

Each discrepancy will be named as an exception and will have a certain code to denote its impact on the loan file. The discrepancies (exceptions) are rated starting from exception #1, being a minor exception to exception #3 being a major exception.

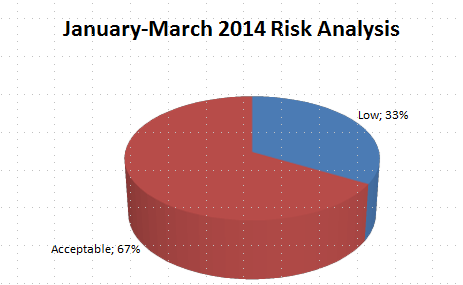

Example of a monthly risk analysis chart.

We will risk score each loan that comes through for review. The analysis

will be based on the exceptions noted during the review and they are

as follows: Low, Acceptable, Moderate & Material Risk.

Risk Analysis is then used to determine the percentage of moderate-material risk loans that are produced yearly and to determine the amount of training and/or corrective actions are needed. |

|

|